March 2025, Western Uganda. An accountant at a private university sat nervously across from our team at Summit Consulting Ltd. He had just been suspended after UGX 320 million “disappeared” from the student bursary fund. No break-ins. No armed robbery. Just clean transactions. The accounting software showed no anomalies. Emails looked legit. Bank instructions were well-formatted. Until we imaged his hard drive. And found one folder, hidden, encrypted, but not invisible. Inside? Fraudulent payment templates, fake approval emails, and a WhatsApp backup of voice notes planning the heist. Because in modern investigations, every byte tells a story. And we? We know how to read them. The digital battlefield. Where lies try to hide Let us stop pretending fraud only happens on paper. Today, most crimes start, pass through, or end on a digital device. Whether it is: An email pretending to be the CFO authorizing payment, A staff phone used to send screenshots of cheque approvals, or A USB drive transferring procurement files after hours, There is one truth: data does not lie. People do. Digital forensics is not about hacking. It is about truth retrieval. We do not crack systems, we unearth intent. The ghost laptops of Ntungamo In late 2023, a district local government procured 150 laptops “for schools.” All documentation seemed clean. Payments cleared. Supplier paid. Except, none of the schools received a single machine. Where were the laptops? We were called in. Here is what digital forensics exposed: Suspicious network history. We requested the supplier’s network logs (they hosted a “track & deliver” portal). There was no record of any delivery schedule after the invoice was paid. Staff call and text metadata. Suspect 1 (procurement officer) had regular late-night chats with Suspect 2 (supplier) during the week the laptops were “received.” Deleted Excel inventory logs. We recovered an old version of the inventory file from the finance officer’s laptop showing only 25 laptops, with handwritten edits attempting to inflate figures. Mobile money analysis. A UGX 30 million Mobile Money transfer traced back to a school bursar’s side-line Airtel line. Purpose? Silence. Laptops were real. Delivery was fake. The data told the story. And that is the power of bytes, they testify even when people lie. Why digital forensics matters today Crimes are going digital. Over 80% of fraud in Uganda today involves digital touchpoints: bank transfers, emails, mobile money, and messaging apps. Evidence is fragile. One reset button on a phone can wipe chat logs. But with forensic imaging, we can retrieve even deleted or encrypted files, legally and accurately. Investigators must evolve. Old-school interviews and ledgers no longer cut it. Today’s investigator needs tools like Cellebrite, FTK Imager, and AI-driven anomaly detection. Tools of the digital investigator Tool Purpose Example FTK Imager Disk imaging Clones staff laptops without altering evidence Cellebrite Mobile extraction Recovers deleted WhatsApp messages, call logs Autopsy File carving Rebuilds deleted documents, photos, PDFs X-Ways Registry analysis Tracks USB history, program installations SummitAI Patterns Behavioural fraud detection Maps unusual activity across staff and vendors At Summit Consulting Ltd, we combine these tools with local fraud context. Why? Because fraud in Uganda does not follow textbook rules, it follows culture, silence, and shortcuts. Key wins from recent investigations School fees manipulation. Traced a bursar who rerouted UGX 94m in “student overpayments” into her brother’s number using disguised Airtel float agents. Procurement collusion. Recovered Dropbox logs showing that three staff shared pricing templates before a sealed bid opening. Email tampering. Found backdated CEO approvals using Microsoft Outlook metadata and mail server logs. Each of these wins did not start with a confession. They started with bytes, suspicious Excel macros, odd file save times, and pattern breaks in normal digital behavior. Why most companies miss the signs Lack of digital audit trails. No monitoring of flash drive usage, downloads, print logs, or unauthorized installations. Weak mobile policy. Staff transact major approvals via WhatsApp with no formal backup. Fraud thrives here. No incident response protocol. When fraud is suspected, devices are wiped or reused before forensic imaging. Reactive, not proactive. Investigations begin after the money is gone. Forensics should be running before, not after. What your organization must do, now Deploy digital forensics readiness plans. Your IT and audit teams must know how to respond to digital red flags without contaminating evidence. Back up with forensic retention. Daily snapshots of key staff computers and phones allow time-machine-style recovery during probes. Train your internal auditors in digital evidence. Most auditors miss fraud because they don’t check browser history, metadata trails, or shadow volumes. Integrate AI anomaly detection tools. SummitAI Patterns learns your staff’s baseline behavior, so it knows when someone suddenly becomes a thief. Data is the new witness. It remembers every keystroke, every click, every WhatsApp reply, every “deleted” file.It does not lie. It does not forget. It does not panic. You can fire a staff member. You can erase an email. You can even throw away the device. But the story has already been written, in bytes. And when we come in, we don’t guess. We read the story your data told behind your back. Byte by byte. Truth by truth. Suspect digital fraud in your institution? Freeze the device. Call Summit Consulting Ltd. Because every byte tells a story. And we’re the ones trained to read it.

Erase All You Want: Forensics Will Find You

Setting: A dusty, humming office in Lira District. A procurement officer leans over her computer and clicks “Shift + Delete.” No Recycle Bin. No trace. She sighs with relief. That was the doctored invoice. Gone forever. Or so she thought. What she did not know is that her machine had already betrayed her. Because in 2025, you can erase all you want, but forensics will find you. And when Summit Consulting’s digital forensics team walks in, they do not ask what happened. They ask, “Where did she hide the truth?” The illusion of digital disappearance Fraudsters in Uganda, especially internal ones, have become bolder, but not smarter. They believe that if they delete Excel files, format flash disks, reset phones, or wipe company emails, the crime disappears. Here is what they do not get. Deleting is not erasing. In digital forensics, deletion is like hiding a body in the garden. We bring the shovel. And the dogs. Case file: The missing purchase order in Soroti In December 2024, a district local government processed UGX 154 million for “emergency borehole repairs.” But an internal whistleblower raised an eyebrow: the works were “done” over a weekend… during a public holiday… with no field reports. Summit Consulting Ltd was called in. When we checked the procurement officer’s laptop, the folder named Q4 Projects had been “permanently deleted” the night before the auditors arrived. Classic panic move. We imaged the hard drive using FTK Imager, cloned the disk, and within four hours: We recovered the original purchase order, it had been deleted but not overwritten. Metadata revealed it was modified 11 minutes after the payment request was submitted. Email logs (yes, even deleted emails!) showed a thread with Suspect 2, a contractor who had never stepped on-site. When confronted, the officer said: “I thought if I deleted it, no one would know.” She was wrong. What digital forensics really means It is not about passwords. It is about patterns. Here is how we catch you: File carving. Recovering deleted files by reading raw disk sectors, even after format. Metadata timeline mapping. Every document carries invisible timestamps: created, edited, accessed, and deleted. USB device history. We know what flash drives you plugged in, and when. Even if the flash drive is gone. Internet activity logs. Your “private browsing” is not private to a forensic analyst. Email header analysis. Shows whether an email was spoofed, scheduled, or forwarded silently. In one ministry, a fraudster emailed a doctored contract, then deleted it. We still found it, in her printer cache. Because even your printer can betray you. The mobile money trap: You can run, but not from CDR In a recent payroll ghost fraud case in Wakiso, we traced suspicious salary transfers to the same Airtel number. When confronted, the suspect claimed: “That line is not mine. I do not know whose it is.” Too bad. We pulled Call Detail Records (CDRs), matched the SIM to tower pings, then cross-referenced it with a phone that had been connected to the office Wi-Fi for the past six months. We found WhatsApp chats, Google location history, and even a selfie backed up on Google Photos, all pointing to one staff member. You can change the line. But your behavior leaves footprints. Why most fraudsters get caught, eventually You see, human beings are terrible at covering their digital tracks. They forget: Windows keeps shadow copies. Phones sync to the cloud. Deleted WhatsApp chats can still exist on the recipient’s phone. Google and Apple track locations passively. In a recent NGO case, a suspect tried to cover her travel fraud by deleting emails and screenshots of flight bookings. We did not even need her phone. We subpoenaed her Gmail account and retrieved flight confirmations from the trash bin. They had been “deleted” but not purged. What you should know if you are tempted to tamper Hereis the digital truth: You try to… We can… Delete files permanently Recover them via file signature carving Format your phone Clone the eMMC and extract partitions Use fake emails Trace headers, IPs, and device signatures Uninstall software Retrieve uninstaller logs and registry Send secret messages Recover from app data backups or caches The more you try to erase, the more fingerprints you leave. You are not outsmarting the system. You are feeding it evidence. How to protect your organization from “digital bleach” Lock device policies. Only authorized devices can access finance systems. Everything else gets blocked. Daily backup with forensic snapshots. Use backup tools that store tamper-proof snapshots. So even deleted files live in the shadows. User behavior analytics (UBA). AI models watch staff behavior for anomalies: who’s deleting too often, transferring late at night, or installing suspicious software. Staff digital integrity profiling. Before promoting or assigning sensitive roles, screen for digital risk behaviors: file hoarding, private email use, unencrypted USBs, etc. Immediate forensic response teams. If you smell fraud, freeze the devices. Don not let IT “clean” anything. Lock it. Image it. Investigate it. Fraud used to wear a ski mask. Today, it hides in Excel sheets, vanishes in mobile phones, and sneaks through Gmail drafts. But no matter how clever the fraudster, forensics is always smarter, because data has a memory deeper than guilt. So here is my advice to anyone tempted to cover their digital sins: Do not delete. Do not format. Do not wipe. Because every click you made… Is already evidence.

USBs and betrayal: The small devices behind big data leaks

USBs and betrayal: The small devices behind big data leaks They fit in your pocket. But they can sink an empire. In April 2025, a mid-tier institution in Kampala found itself in crisis. Over 13,000 client records including national IDs, claim details, and medical histories, were leaked to the dark web. At first, the firm suspected a cyber breach. Sophisticated hackers. Maybe a compromised firewall. But the truth was more primitive. More personal. It came in the form of a 16GB SanDisk USB drive. And the betrayer? Not a foreign agent. Not a hoodie-wearing hacker in Moscow. Just “Susan,” a long-trusted compliance officer, who’d been working there for six years. This is how betrayal hides in plain sight, and how tiny USB sticks are still causing the biggest data disasters in Uganda. The USB, a perfect weapon for insiders USB drives are cheap, silent, and easy to hide. Unlike cloud storage, they do not trigger alerts. No login required. No audit trail. Just plug, drag, eject, and vanish. In the Summit Consulting Ltd forensic lab, we call them “digital boda bodas.” They ferry sensitive information out of organizations quietly, invisibly, and often under the noses of IT departments. What a VPN and hacking toolkit take hours to execute, a USB does in seconds, with no logs to trace. The insurance leak that exposed thousands Here is how it happened. (i) Motive: Susan was under financial pressure. Her brother had defaulted on a loan. A local loan shark offered her UGX 2 million in exchange for “high net worth client data.” (ii) Opportunity: Susan had access to claim reports for compliance checks. She would download monthly backups to her machine. Nobody questioned her, it was part of her job. (iii) Execution: On April 7th, she plugged in a generic USB stick during lunch hour, copied 14 Excel files, renamed them “School Photos,” and tucked the device into her bag. (iv) Cover-up: She deleted the recent file history and cleared the USB logs using freeware she downloaded on her personal laptop. Two weeks later, an anonymous Telegram account began leaking the data. It was sold to fraudulent claim processors and ID forgery syndicates. We were brought in after fake claims started flooding the company. It took just 22 minutes to copy the data. But it cost the company UGX 920 million in regulatory fines, fraud losses, and brand damage. Why USBs remain the ultimate betrayal device You might think USBs are obsolete. After all, we are in the cloud age, right? Wrong. They are still the go-to tool for: (i) Whistleblowers: Genuine or malicious, trying to extract files without alerting the system. (ii) Disgruntled employees: Especially those exiting or under investigation. HR rarely checks devices during exit interviews. (iii) Contractors and IT staff: With temporary access and low oversight, they often plug in tools for “maintenance” that double as data siphons. In one case in Jinja, an IT intern cloned the entire HR folder of a sugar processing firm by installing a USB syncing tool that auto-copied files every time he plugged in. The blind spot in most organizations Most companies in Uganda focus on firewalls and anti-virus tools. But the real risk is port-based. Your data doesn’t always leak via the internet it walks out through USBs, one stolen file at a time. In audits done by IFIS/ SCL across 12 organizations in 2024, we found: (i) 80% had no endpoint control over USB access. (ii) 67% allowed personal USBs on work machines, no approval, no encryption. (iii) Only 2 had automatic USB activity logging. How investigators cracked the insurance case It was not Susan’s name that gave her away. It was the metadata on the Excel files (yes, metadata again) that pointed to her user account. But what sealed the case was USB registry artifacts, hidden in Windows Event Viewer logs. With forensic software, Summit Consulting reconstructed her file transfer timeline: USB inserted at 12:38 p.m. File transfers between 12:39 and 12:58 p.m. Ejection at 12:59 p.m. She denied it. Until we presented video footage showing her plugging in the device. She folded. Red flags every business must watch (i) Employees refusing to use cloud drives and preferring “offline work.” (ii) Staff staying late alone with access to servers. (iii) Sudden interest in files outside their job role, especially large datasets. (iv) USBs found in unusual places: under keyboards, in drawers, or even in ceiling tiles (yes, we’ve found them there). Total cost of betrayal The firm lost more than money. (i) They lost clients. (ii) They lost trust. (iii) They lost a 12-year no-breach record. A 16GB USB stick cost them UGX 920 million. 3 actions to take right now Lock down all USB ports. Use endpoint protection tools like Symantec DLP or Device Control to whitelist approved devices only. Enforce encryption. Every allowed USB must be encrypted, and all data copied should require clearance and tracking. Run surprise audits. Periodically scan workstations for USB activity logs and compare against approved device lists. Tiny device. Titanic damage. If you are still thinking, “It is just a flash drive,” you have already lost the war. The modern data leak does not start with a hacker. It starts with someone you trust. Someone with access. Someone with a USB. Trust, but verify. Block, then allow. Monitor, always. In the end, betrayal does not come through the front door. It walks out of your building, hidden in someone’s bag. And it only takes 22 minutes. The role of forensics in insider threat investigations Insider threats do not wear masks. They wear your company badge. They attend your morning meetings. They sign your HR policies. They greet security on the way in, and steal your crown jewels on the way out. But how do you catch them? You do not chase. You trace. And that is where digital forensics comes in. It is not about intuition. It is about irrefutable evidence, the kind that speaks even when suspects stay silent. What

Metadata matters: What your files reveal without saying a word

It is not the file you send. It is what is hidden inside it. Every time you share a document, photo, or spreadsheet, you may be disclosing more than you intended. Not in the text. Not in the numbers. But in the metadata, the invisible fingerprints your files carry. That “final_report_v3.docx” you emailed last week? It might tell your boss that you were not the author. Or that it was edited at 2:43 am, by someone else. That PDF you uploaded to the regulator? It might include your GPS coordinates. Your internal network name. Even the username of the junior officer who typed it. Metadata does not lie. It tells when a file was created. Where it was edited. Who opened it last. How long they spent on it. It is the digital equivalent of body language, subtle, subconscious, and often more revealing than words. Why this matters for your organization In fraud investigations, metadata has become a goldmine. Investigators from Summit Consulting Ltd recently cracked a procurement forgery ring after noticing that multiple bid documents, supposedly from different companies, had identical author metadata, same username, same creation timestamp, same font template. The fraudster? An insider from the procurement team. In a court of law, improperly scrubbed metadata can sabotage your entire case. You redact the names in a whistleblower report, but the metadata still shows the original filename “Complaint_by_John_K.pdf”. You may think you are sending a clean file. You are not. In one audit of a government agency, the internal audit team flagged multiple suspicious payments. But what broke the case open was metadata from Excel files attached to fake invoices. Each invoice claimed to be from a different supplier. But the file properties told another story. All had been saved from the same laptop under the same Windows account “admin_kintu”. Another time, a leaked PDF report from a high-profile SACCO scandal caused panic when journalists discovered metadata showing the document had been authored by the SACCO’s own legal officer despite public statements denying any internal involvement. Three metadata traps to avoid today Blindly forwarding files. When you forward a Word or Excel document, you are forwarding its entire edit history. Who made what changes. And when. Sometimes, even deleted comments reappear when opened in different versions. Uploading documents without scrubbing. Every upload to a website, shared drive, or third-party regulator submission should go through a metadata scrub. Otherwise, you might be leaking internal usernames, drive paths, or sensitive workflow history. Over-reliance on redaction tools. If you redact a file in Word or PDF using normal highlight-delete, the metadata (and sometimes the previous versions) are still embedded. You must flatten or sanitize the file using forensic-grade tools. What you must do now You need a metadata awareness policy. Not just for IT. But for everyone who sends, shares, edits, or uploads documents. At Summit Consulting Ltd and IFIS, we recommend three layers of defense: (i) Train your staff. Metadata risks must be part of cybersecurity and fraud awareness training. Do not assume knowledge. (ii) Deploy automated tools. Tools like Metashield or cleanDocs can scrub documents before they are emailed or uploaded. Automate hygiene. (iii) Build metadata review into your investigations. Every fraud investigator must know how to extract metadata and use it to correlate evidence. It is the new fingerprint. Metadata never forgets In the age of digital forensics, every file is a potential witness. And metadata is the diary it secretly keeps. You would not walk into a courtroom with your home address written on your forehead. So why submit files with invisible trails pointing right back to your desk? Clean before you send. Or risk revealing more than you know.

DIGITAL FORENSICS QUIZ

Think you can trace digital footprints, uncover hidden evidence, or spot cybercrime like a pro? Take this quick but revealing quiz and test your forensic instincts, you might be smarter than a hacker… or you might be leaving clues behind without even knowing it. Only one way to find out, dive in, follow the digital trail, and uncover what your instincts are made of. SCORING GUIDE Score Range Level Interpretation 90–100 Expert You have strong digital forensics skills and can support or lead investigations. 70–80 Proficient You understand key concepts well, but need more hands-on practice or tools use. 50–68 Developing You grasp the basics but may miss subtle details in real investigations. 30–48 Beginner High risk of oversight in forensic-sensitive environments. Needs full training. Below 30 High risk Unfit to handle digital evidence without supervision. Must attend foundational course. Level: Basic to Intermediate Total Questions: 25

Data breach in 30 seconds: Can your business survive a real-time cyber attack?

The war room is an interesting place – you get to see everything in action. The iShield360 cybersecurity center monitors all client traffic in real time. The breach that started with a beep It was exactly 2:13 AM on a Sunday in March 2025 when a small hospital in Mukono received a strange notification: “System Exception: Connection timed out from External IP 102.244.XX.89.” The IT officer ignored it. Assumed it was an internet blip. By 2:43 AM, the attackers had taken full control of the Electronic Medical Records (EMR) system. By 3:01 AM, every patient file had been encrypted. By 3:12 AM, a ransom note was displayed on every computer: “We control your data. Pay UGX 180 million in Bitcoin within 48 hours or say goodbye to your hospital.” The breach lasted less than 30 minutes. But the impact? Catastrophic. How it happened: A perfect digital storm The entry point? A smart printer is connected to the same Wi-Fi as the hospital’s core systems. No password. No segmentation. Just wide-open access. Attackers scanned the Ugandan IP space for unprotected devices. They found the printer, logged in via its default admin panel (admin/admin), and used it to move laterally. Within minutes, they were in the EMR. No firewall rules. No endpoint detection The antivirus? Expired. The patching? Incomplete. The backups? Stored on the same network they just hijacked. This wasn’t a hack. This was a walk-in robbery, with the doors left open and lights turned off. The anatomy of a 30-second breach a) Stage 1: Reconnaissance (10 seconds) Attackers used a mass IP scanner. Within seconds, they identified a vulnerable IoT printer. b) Stage 2: Exploitation (5 seconds). They accessed the printer dashboard, opened SSH, and dropped a payload. c) Stage 3: Privilege escalation (5 seconds). They found hardcoded credentials stored in a plaintext config file. Full admin access achieved. d) Stage 4: Lateral movement (7 seconds). They jumped to the EMR server. No multi-factor authentication. No logs. No alerts. e) Stage 5: Encryption and exfiltration (3 seconds). A custom ransomware payload ran. Files encrypted. Copies of sensitive patient data were uploaded to an offshore server. Time to total lockdown: 30 seconds. The cost of silence For five hours, the hospital operated on guesswork. Nurses could not retrieve patient histories. The lab couldn’t match the samples. Doctors couldn’t issue prescriptions. Operations were postponed. A diabetic patient suffered complications because no one could verify the insulin dosage history. The hospital ended up paying the ransom out of pocket. But the data was never fully restored. Reputation? Shattered. Compliance? Violated. Trust? Gone. Can your business survive a real-time attack? You don’t need to be in a hospital. You could be a SACCO, an accounting firm, or a courier company. If you depend on data and your systems are exposed, you’re next. Let’s test your readiness right now: a) Can your team detect an abnormal login at 2:13 AM? b) Are your backups disconnected from your core network? c) Do your printers, CCTV, and access systems have unique, hardened credentials? d) When was your last red team simulation? e) Who is your incident commander during a breach? If you can’t answer confidently in 10 seconds, then a hacker already has a head start. Summit’s incident response: The digital firefighters When Summit Consulting was called, our first question wasn’t “what happened?” It was: “Where is the breach still hiding?” We isolated the infected subnet. Activated Summit iShield360 threat containment. Traced the ransomware signature to a variant from a known East African cybercrime syndicate. We initiated dark web monitoring to track the leaked data. But by then, the damage was done. The lesson was clear: Response is not prevention. Preparedness is everything. Why most businesses fail to respond Because they assume “IT will handle it.”But cybersecurity is not IT. It’s governance. And it must be treated as a board-level risk, not a technician’s side project. Most Ugandan companies don’t even have an incident response playbook. They wait for fire, then call for water, when the entire building is ash. The new rule of business survival Forget fire drills. You need breach drills. Your team should rehearse a ransomware response just like a heart attack resuscitation. And your systems must follow the five rules of digital hygiene: Segment everything Monitor continuously Patch religiously Backup offline Train without ceasing Real-time cyberattacks don’t wait for board approval. They execute. Automatically. Closing thoughts: Your countdown has already started If an attacker had 30 seconds to bring your business to its knees, would they succeed? Think carefully. Because they already have the tools. The only question is whether you have the discipline, visibility, and strategy to stop them. As Mr Strategy, I leave you with this: Cybersecurity is no longer about if. It’s about when, how fast, and how deep. And in this new era of weaponized code and AI-driven attacks, speed is your only defense. Prepare like your business depends on it because it does. Or call us after the breach, if you’re still standing. IFIS Team.

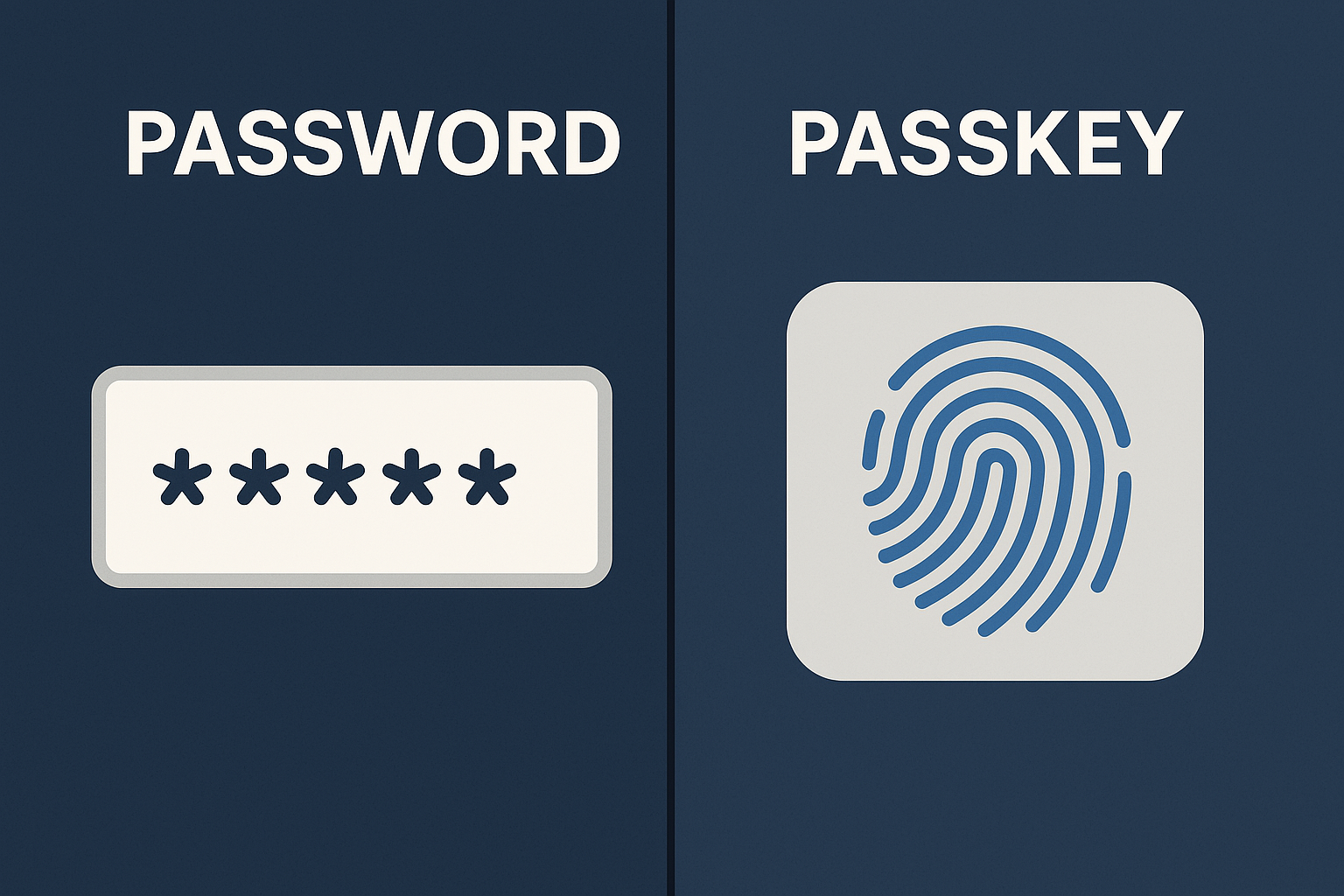

From passwords to passkeys-the future of digital identity

It all starts with a compromise It always begins with a password. In June 2024, a procurement officer at a large local firm used the same password, Brenda@2020, across her Gmail, Zoom, and company ERP. She thought no one would care. But someone did. A hacker running a darknet scraping tool picked it up from a 2021 data breach dump. Within hours, they were in. Not just into her Gmail. But into internal payment systems. The hacker didn’t break down a door. He walked in with a borrowed key. This is not just about weak passwords. It’s about passwords themselves. They’ve become the single point of failure in our digital lives. The password paradox Passwords were invented in the 1960s. But in 2025, they’re still guarding trillion-shilling systems, despite being laughably outdated. Here’s the paradox: The stronger your password, the harder it is to remember. The easier it is to remember, the easier it is to hack. This gives rise to the three horsemen of digital doom: Re-use. Predictability. Social engineering. You can have the best firewall, but if your HR manager is using Godisgood@123, you’re a ticking time bomb. The phasing out of passwords: Enter passkeys The future is passwordless. Tech giants like Google, Apple, and Microsoft have adopted passkeys, cryptographic credentials that never leave your device. Instead of typing a password, you use your fingerprint, face, or device PIN. The secret never travels across the internet. So it can’t be phished, stolen, or brute-forced. Think of passkeys as digital locks with no keys. Only your face or finger can open them. But here’s the real power: zero knowledge architecture. The server doesn’t even store your credentials. No more vaults to break into. No more passwords to leak. What makes passkeys better a) They’re phishing-proof No one can trick you into “entering” a passkey. Because you don’t enter it. You just verify. b) They’re seamless Log in to your banking app with Face ID? That’s a passkey in action. c) They’re device-bound Your biometric data never leaves your phone. That means even if a hacker breaches the server, they get nothing. This is a paradigm shift from “what you know” (passwords) to “what you are” (biometrics). So why are we still stuck in 2005? Because enterprises are slow. In Uganda, most government systems still run on basic login forms, sometimes with no multi-factor authentication at all. Banks preach security, yet allow 4-digit PIN resets over the phone. And SMEs? They share passwords across departments like they’re sweets. Passkeys threaten not just bad habits, but entire business models built on selling password managers, OTP tokens, and ‘user support’ services. This change isn’t just technological. It’s cultural. And culture resists change. A real-world case: when a bank chose wrong Summit Consulting was called to investigate a breach at a digital-only bank in East Africa. An insider used an old employee’s credentials, still active, to access backend systems. Why? Because no one had enabled biometric authentication or zero-trust policies. No device binding. No session expiry. Just passwords. One compromise. UGX 1.2 billion lost. In three transactions. A system that depended on trust and static passwords was no match for modern fraud. The future– digital identity without friction Imagine this: You walk into your office. Your workstation unlocks automatically when your watch comes within 2 meters. Your payroll system recognizes your face. Your access to sensitive documents is time-bound and geofenced. That’s not sci-fi. That’s passkey+contextual authentication. And it’s already here. The future of digital identity is invisible security. Seamless to the user. Brutal to the attacker. Why CEOs must care now Passwords are not just an IT issue. They’re a boardroom risk. Every fraud case I’ve handled in the last 18 months has had one thing in common: Credential compromise. Yet most leaders still rely on “change your password every 90 days” as a security policy. That’s like changing the padlock every month while leaving the door wide open. Passkeys eliminate the human error factor. They reduce helpdesk costs. They improve compliance. More importantly, they reduce fraud exposure by design. Closing thoughts-Kill the password before it kills your company If your organisation is still relying on passwords in 2025, you’re not behind the curve. You’re inside the breach. As Mr Strategy, I say this with brutal clarity: Password policies won’t save you. Passkeys will. Make the switch. Mandate biometric sign-ins. Train your staff on behavioral phishing, not just “IT policy.” And above all, never let digital identity be an afterthought. Because identity is the new perimeter. And if your walls are weak, you won’t know you’ve been breached—until it’s too late. Let Summit Consulting help you cross that bridge. Before someone else burns it down.

The Silent Threat, How phasing attacks are outsmarting even the smartest employees

One Wednesday morning in August 2024, the Finance Director of a top-tier insurance company in the region clicked an email that looked perfectly ordinary. The subject was “Request for Approval—Updated Q2 Premium Report.” It had come from what appeared to be the CEO’s personal Gmail. She clicked. The screen flickered. Then, it froze. That was the first move in a highly coordinated phasing attack. Not phishing. Phasing, a more sophisticated, patient, and devastating evolution of social engineering. Unlike classic phishing, where attackers bait you into clicking suspicious links, phashing is a silent predator. It slowly infiltrates, studies, and mimics internal behaviors, gradually earning trust before making a move. No Nigerian prince. No spelling errors. Just perfect timing and familiarity. AI has transformed business models of fintechs and criminals alike! From infiltration to impersonation The initial breach began two months prior. One of the IT interns, keen and talented, had reused a weak password from his university email. That same password had been compromised in a 2023 LinkedIn breach. The attacker didn’t rush. He monitored internal communications for 49 days. He studied the nicknames staff used for each other. Observed workflows. Noted when key decision-makers were on leave. The hacker didn’t hack—he blended in. Then came the masterpiece. The attacker crafted a perfectly worded email chain that mirrored prior correspondence between the CFO and the Managing Director. He spoofed the domain using lookalike techniques. insureafrica.com became insure-áfrica.com. The “á” was a Unicode character. Visually identical. Technically different. The attack unfolds By the time the fraudulent payment request landed in the CFO’s inbox, the attacker had even copied her writing style, using past emails. The attached Excel file wasn’t malware. It was clean. But the bank details inside had been phased in gradually over a week of supposed “update” emails from the fake MD. The instruction was simple: “Please wire $184,600 (UGX 700 million) to our offshore reinsurance partner to beat the compliance deadline.” The urgency made sense. The tone was spot-on. The signature? Flawless. Three days later, the company’s real MD returned from a strategic retreat. He asked, “Have we paid the Swiss reinsurance team yet?” That’s when the silence broke. What is a phasing attack? Phasing is the fraud triangle on steroids. It combines: a) Deep reconnaissance: The attacker lives inside your digital system undetected, studying patterns and behaviors. b) Gradual manipulation: Small, innocuous changes are introduced over time—modified vendor records, subtle domain changes, new rules. c) Perfect social mimicry: The fraudster doesn’t attack your firewall. He attacks your mind by acting exactly like someone you trust. This is no longer about bad grammar. This is about behavioral cloning. The red flags they missed Summit Consulting Ltd was called in after the breach. Our digital forensics team discovered five critical signs that were overlooked: a) The fake domain was registered just 3 weeks before the incident. A basic domain intelligence tool would have flagged it. b) The intern’s credentials had been used to log in from two IP addresses in Brazil and Bulgaria. No geo-restriction rules had been set. c) The “updated bank account” had replaced a previously verified local account. No dual approval rule was triggered. d) The company had disabled 2FA (Two-Factor Authentication) temporarily for “email migration” and forgot to reinstate it. e) Finance staff did not cross-verify the payment via voice call—a standard protocol buried in dusty policy binders. The anatomy of the loss UGX 700 million vanished into a crypto exchange in Slovenia. The money was converted within 48 hours and broken into dozens of wallets, then funneled through a chain of obfuscation layers on the dark web. Suspect 1, a shadowy regional cyber-mercenary, had used local mules to cash out. Suspect 2, believed to be a university dropout with a history of web scraping projects, created the spoofed domain and communications templates. They never stepped into the building. But they had lived inside the systems—and minds—of the organization for two months. The silent threat becomes a loud lesson Summit’s final report was sobering. Internal controls were there. But they were outdated, ignored, and poorly enforced. The organization had: No active cyber threat monitoring tools. No employee behavioral training on deep social engineering. No incident response playbook. The loss, 700 m+, was uninsured, unaudited, and entirely preventable. Why smart employees still fall Because intelligence is not immunity. Phasing attacks don’t exploit ignorance. They exploit trust, busyness, and routine. Even the best-performing staff fail when the system is silent, and the threat is cloaked in familiarity. It’s not stupidity that gets you hacked. It’s predictability. Cracking the case-How Summit unraveled it Our team used Summit iShield 360, a proprietary suite of forensic tools, to trace the attack vectors. We triangulated metadata from emails, accessed admin logs using preserved timestamps, and reviewed DNS history. We found the point of initial contact. The intern’s compromised account. From there, we reconstructed the attacker’s timeline using log correlation. The breakthrough came when we linked a WhatsApp number, used by the fake reinsurance “agent”, to a delivery order of an iPhone in Jinja. A careless digital breadcrumb. That’s all we needed. Your biggest vulnerability wears a name tag Technology doesn’t fail. People do. Your systems are only as strong as the culture they operate. If your internal processes are based on trust instead of verification, you’re not secure- you’re just lucky. As Mr Strategy, I say this: Train your staff like soldiers. Test your systems like hackers. And treat every email as a loaded gun. Because in this new world of silent digital warfare, you don’t get a second chance. Final loss: UGX 704,378,100. One careless click. Two months of quiet surveillance. Three actors in play. And just like that, gone. But not forgotten. The war continues. IFIS and Summit Consulting remain on the front line.

AI vs AI: Fighting fraud with the same weapon fraudsters use

AI vs AI: Fighting Fraud with the Same Weapon Fraudsters Use Scene: Ntinda, Kampala. March 2025. A junior accountant receives a WhatsApp message: “Hello, Finance, this is the CEO. Urgent supplier payment needed before COB. Here’s the account. Process now.” The logo on the profile photo was legit. The tone? Perfectly matched. Even the CEO’s usual “Thanks, team” signature was there. It was fake. Generated by AI. And within 2 hours, UGX 46 million was gone. Welcome to the era of AI vs AI, where the same algorithms used to defraud you are now being weaponized to protect you. But here’s the kicker: most Ugandan firms are defenseless. From Deepfakes to Deep Fraud Fraud is no longer about forged signatures and disappearing vendors. It’s about machine-powered deception. We’re facing fraudsters who use: Voice cloning – 20 seconds of your CEO’s voice can create a believable request for payment. ChatGPT-like phishing bots – Auto-generate personalized scam emails that sound like they’re from your HR or IT team. Synthetic identity fraud – AI combines real and fake data to create “legit” employees or suppliers in your system. It’s no longer “catch the thief.” It’s “outsmart the algorithm.” And here’s the twist: AI can also fight back. But only if you let it. The NGO that fought fire with fire In late 2024, a prominent donor-funded NGO in Gulu noticed strange activity: Staff travel claims were submitted for trips that had no supporting evidence. Fuel claims had GPS coordinates in Kenya instead of Uganda. Something was off. Summit Consulting Ltd was called in. We deployed SummitAI Forensics, a machine-learning model trained on prior fraud cases, and cross-referenced travel claims against: Mobile money geolocation patterns WhatsApp call logs metadata GPS engine data from staff vehicle trackers Within 36 hours, the system flagged five red alerts. One staff member claimed to be in Mbale while their phone had connected to a tower in Bunga. Another had two overlapping claims filed within 12 minutes of each other, across districts. AI didn’t just detect anomalies. It exposed behavior patterns humans had missed for months. Fraud caught. Losses contained. What traditional systems miss Excel can’t fight AI. Your finance team’s internal controls can’t match the speed of a script that generates 100 fake invoices in under 2 minutes. Here’s what you’re up against: Fraud Tactic Powered by Traditional weakness Fake voice memos from “CEO” Voice AI Lack of verification protocols Vendor impersonation Chatbot + LLM No cross-check against known supplier data Synthetic staff profiles Deep learning + public records Poor HRIS integrity Insider collusion detection Network anomaly analysis Human auditors overlook patterns Travel & fuel fraud AI-generated itineraries No GPS or AI correlation tools The enemy is using automation. And you’re still using approvals on WhatsApp. Fighting back–How to deploy AI defensively Behavioural analytics over approvals AI doesn’t need an approval form, it watches for deviations. Who paid what, when, from where, and how often. If it’s not normal, it alerts. Instantly. Voice verification firewalls Implement voice signature match tech. If your CEO’s voice is cloned, it won’t match the signature stored. That’s AI detecting AI. AI-augmented internal audit Train your internal audit team on AI-powered risk models. Feed your past frauds into a model and let it flag future patterns automatically. Smart vendor onboarding Use AI to check for red flags like duplicate TINs, shell companies, fake physical addresses, and recycled phone numbers. Employee lifestyle AI tracker When salaries don’t match iPhone purchases or weekend travel patterns, the system flags a risk. Not for judgment, for investigation. Uganda’s advantage – We leap when we lag Paradoxically, Uganda’s late adoption of traditional tech gives us a leapfrog chance. While Europe is bogged down by GDPR compliance delays, we can implement lean, smart AI-driven controls fast, if leadership permits. This is not about replacing people. It’s about arming your people with a smarter co-pilot. What SummitAI is doing Summit Consulting Ltd has developed an AI-driven fraud detection tool trained on real Ugandan fraud cases from over 100 institutions. It understands local fraud behavior: The “Monday–Friday” financial fraud schemes The boda-boda travel reimbursement fraud The “we bought but didn’t receive” procurement hustle The mobile money laundering loop via school fees or airtime purchases We don’t rely on foreign data models. We use Uganda’s financial crime history to fight tomorrow’s attacks. AI isn’t just coming. It’s already inside your finance department, your HR, your procurement, just not on your side yet. You have two choices: Let AI attack you. Or deploy AI to defend you. There is no neutral ground. Because in the next board meeting, when you ask “How did we lose UGX 1.2 billion?”, the answer will be: “We didn’t lose it. We were outsmarted by a machine we never saw.” Act now. Let the Institute of Forensics & ICT Security assess your fraud AI readiness. Contact us, we’ll help you fight code with code. Because in this era, strategy isn’t human vs machine. It’s the right machine vs the wrong one. We remain, Institute of Forensics & ICT Security, 2025. All rights reserved.

Greed, guts, and gone: The human drivers behind every scam

On the sticky floor of a dimly lit bar in Kabalagala, Suspect 1 sealed the deal with a casual handshake. The deal? A multi-million Uganda Shilling “consultancy project” that existed only on paper and in the minds of two co-conspirators, powered by three invisible forces that fuel every scam you’ve ever heard of: Greed. Guts. And eventually, Gone. Let’s break it down. What happened? In April 2024, a high-ranking officer at a government parastatal in Uganda wired UGX 870 million to a company claiming to offer digitization advisory services. The only digitization that happened was converting public funds into personal pleasure. The company? A freshly registered firm run by Suspect 2, whose only experience with “digitization” was editing PDFs. Summit Consulting Ltd was called in after a whistleblower reported that “consultants” were being paid without ever stepping foot in the organization. The fraud was already in motion. But the audit trail had cracks, cracks that eventually became confession points. It starts with greed Greed is the gateway drug of corruption. It always begins with justification. Suspect 1, let’s call him “The Fixer”, had a nice salary, a government car, and a per diem habit. But that wasn’t enough. One evening, he told a friend at Panamera, “Okuyiya kwekuggawaza si musaala,” loosely meaning, “it is dealing, not a salary, that makes a man rich.” So when a dormant procurement budget line showed UGX 920 million unutilized by Q2, he saw opportunity, not mandate. He engineered a fake urgency, “We need digital strategy support”, then co-signed the paperwork to sole-source the work to a “known vendor.” That vendor? A shell company. Just three weeks old. Owned by his cousin. Who also happened to be Suspect 2. Then comes the guts Fraud is not for the faint-hearted. It requires nerves. Precision. And the audacity to say, “Let’s beat the system.” Here’s how they did it: Front company. Registered with URSB with a fake office at a building in Bukoto. Their “office” was a locked storeroom. Invoice engineering. They submitted three inflated invoices, UGX 290m each, under different phases of the so-called project. The descriptions were vague: “Digital Readiness Scan,” “Stakeholder Engagement Sessions,” “Cybersecurity Awareness Roadmap.” Not a single actual deliverable was submitted. But the language was seductive enough to lull the internal reviewers. Internal collusion. Suspect 3, a mid-level accounts officer, ensured payments were fast-tracked. In return? A crisp UGX 30 million Mobile Money transfer, disguised as “school fees support.” It was sent to his wife’s Airtel line. Cash-out strategy. Once funds hit the vendor’s account, they were immediately withdrawn in bits, UGX 50m at a time, using mobile money, cheques to cash, and over-the-counter transactions at a bank in Ntinda. The audit trail vanished under the cloak of informal cash culture. And just like that… gone When the procurement committee asked to review the final report, both Suspects 1 and 2 were “on study leave.” The company had de-registered. The bank account was emptied. The funds were gone. Forever. And yet, it could’ve been caught earlier. The red flags the auditor spotted Vendor vetting was bypassed. The company had no prior contracts, physical inspection reports, or due diligence forms on file, so all were waived under “urgency.” Duplicate language across invoices. Copy-paste errors appeared in all three invoices. Same spelling mistakes. Same format. No deliverables attached. Payments were made without any accompanying reports. Only proforma invoices were filed. Mobile money activity spikes. A suspicious surge in MM transfers by a junior accountant raised eyebrows. One number appeared repeatedly in transaction logs, a number linked to Suspect 2. Unusual speed of payment. Most vendors waited weeks. This vendor was paid within 48 hours. Enter the Summit Consulting Ltd investigation When Summit Consulting Ltd was engaged, the forensic trail was thin. But we started with three things: Bank statements. These revealed transfer patterns and suspicious withdrawal behaviour. Mobile money analysis. We used telco data subpoenas to map all large transfers from the key suspects. Interview triangulation. Using a personality profiling tool and analysis of all staff statements, we flagged inconsistencies in answers between the procurement officer, finance officer, and line manager. It took six working days to map the entire fraud ring. Suspect 2 cracked under pressure. In exchange for immunity, he handed over WhatsApp chats, shared location pins of cash drop-offs, and even voice notes. One voice note from Suspect 1 was chilling: “Make sure the last payment lands before the board meets. I don’t want questions.” The total loss UGX 870 million. Gone into thin air. Money that could’ve upgraded district health centers, or digitized actual village SACCOs, ended up paying for beach plots and imported whiskey. Why it worked– internal controls were ignored Segregation of duties was non-existent – The same officer initiated, approved, and followed up the payment. No vendor onboarding framework – Any company could be selected under the pretext of “urgency.” The procurement committee was a rubber stamp – None of the members even attended the so-called vendor pitch. Finance never asked questions – They processed all payments without checking for deliverables. Board oversight was blind – There was no project performance dashboard or progress reporting mechanism. The human drivers – greed, guts, and gone Every scam begins with greed, a want for more than earned. It escalates with guts, the courage to beat the system. And it ends with gone, vanished money, broken trust, and reputations in ruins. But behind every ghost invoice is a living, breathing human being who looked at ethics and chose expediency. Fraud is not a system failure, it’s a human decision wrapped in paperwork. Fraud doesn’t hide in spreadsheets. It hides in culture. In that silent nod of approval. In that “it’s just this once” excuse. In that handshake in the backroom. Want to beat fraud? Don’t just automate. Investigate your people. Build controls around human behaviour. Reward integrity. Audit lifestyles, not just numbers. Because in Uganda, and beyond, every scam is human. And until you confront greed and guts, you’ll